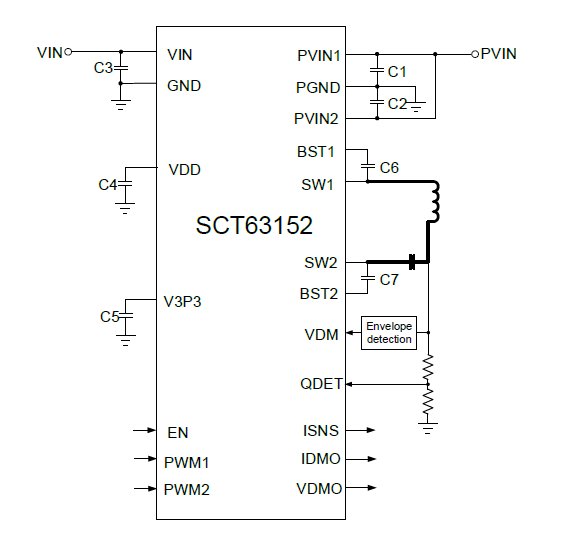

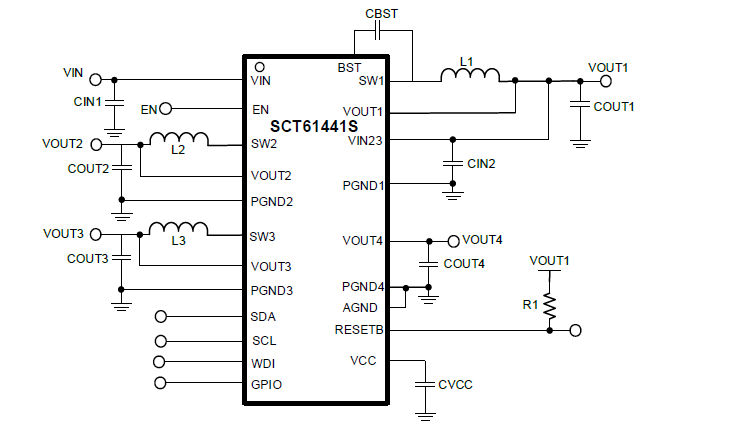

Products

0

0

Power management chips are responsible for the conversion, distribution, detection, and other power management tasks within electronic device systems. Power supply is an essential function for all electronic products and devices. Efficient conversion and safe stability are critical requirements for all power management chips and power devices.

As key components of electronic devices, the performance of power management chips greatly influences the performance and reliability of electronic products, making them one of the largest submarkets in analog chips. The following is an exclusive interview with Liang Junfeng, Deputy General Manager of SCT, based on the "2023 China Power Management Chip Industry Research Report" from Yiou Think Tank:

1. As a major category of analog chips, what are the characteristics of the power management chip industry as a whole, and what breakthroughs or advantages exist in domestic production?

Liang Junfeng: When discussing power management chips, we first need to focus on the application scenarios rather than the chips themselves because power management chips are responsible for power conversion, distribution, and detection within electronic device systems. Essentially, in most cases, they are part of the power supply within a product, so when we discuss power management chips, it should center around the application.

From the overall industry perspective, power management chips have diverse applications, covering industries such as consumer electronics, portable devices, computer communication networks, industrial control and robotics, automotive electronics, medical equipment, and the Internet of Things. The types of chips required vary greatly across these sectors, with significant differences in demand and characteristics.

The challenges faced by domestic power management chips mainly involve two aspects:

Power challenges: Focused on high-power integrated solutions, such as high power density, high efficiency, and high integration power management devices. For example, in the communication industry, power management chips with ultra-high current integrated MOS are still constrained by technological limitations.

Design barriers: For instance, in automotive electronics, products with high functional safety standards require advanced design. In the automotive power sector, achieving high current power switches is still challenging for the industry.

As a domestic semiconductor design company, SCT's breakthrough lies in better serving leading domestic markets and customers, solving technical pain points with clients during development, and persistently developing innovative products that better meet market applications. We recognize that the foundation of the company’s survival and development lies in the quality and reliability of products. We are committed to a quality-centered approach, building a three-in-one quality system that ensures design, reliable manufacturing, and quality control.

2. What characteristics do power management chips have in different application fields, and what are the varying customer requirements?

Liang Junfeng: There are significant differences in demand across industries:

Consumer Market:

The consumer market is currently the largest, with smartphones being the most representative terminal product in consumer electronics. Power management chips must meet the size limitations of smartphones and the user demands for performance enhancement and battery life. Core demands for power management ICs include:

Hence, power management ICs are continually required to improve in areas such as efficiency, size, power consumption, and frequency.

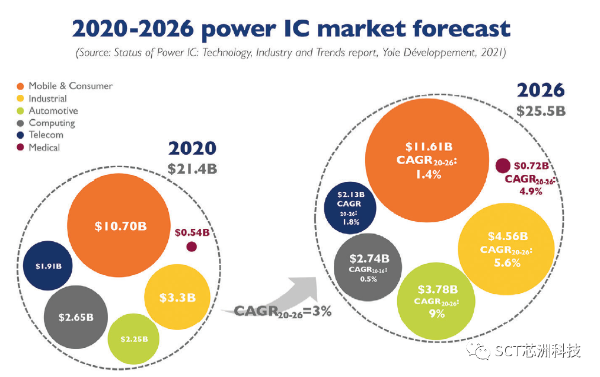

资料来源:status of power IC:technology,Industry and Trends report,Yole Development

Industrial Market:

Each sub-market in the industrial sector has different demands, so it’s similar to the consumer market, where we focus on the most advanced and representative applications. Currently, the focus is on industrial automation, robotics, etc.

The ultimate goal of industrial automation is to improve production efficiency, requiring rapid information response, precision, and speed in the entire control process. Power management ICs must handle very high current while meeting size requirements, so the trend is toward integrated power solutions (PMIC).

For robotics, especially logistics and industrial robots, battery-powered systems (mainly 36V-48V) are becoming the standard. This requires power management ICs to handle voltages up to 100V, supporting more complex power scenarios. SCT offers nearly 20 products in the 100V series to meet various market and application needs, along with high-reliability driver chip solutions.

Automotive Electronics:

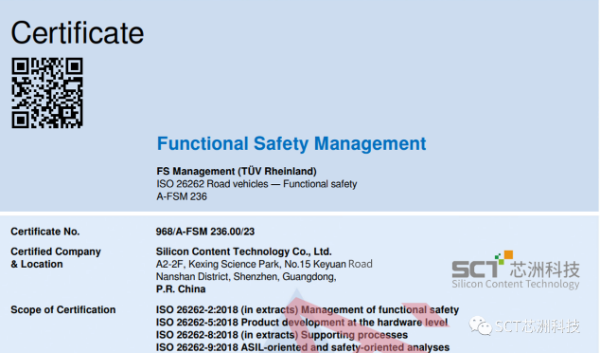

Automotive electronics is a leading industry for domestic semiconductor companies. It is divided into multiple domains such as intelligent cockpit, ADAS, body domain, power domain, and chassis domain. Domestic power management chips have varying coverage across these domains, with coverage decreasing as the domains’ safety requirements increase. Major barriers include process standards and meeting functional safety levels. SCT currently covers 80% of in-vehicle power chip applications and has achieved ISO 26262 functional safety management system ASIL D certification.

Domestic automotive-grade power management ICs focus on DC-DC, LDO, PMIC, etc. With the development of electrification, intelligence, sharing, and connectivity in new energy vehicles, the demand for computing power continues to increase, leading to higher board power requirements, greater power density, better heat dissipation, and improved device interference immunity.

Communication Market:

The communications sector is also a leading area in power management, with demands for high power density, ultra-high frequency, and various other specifications such as integrated power management, system power management, and ultra-low noise LDOs.

Key features of the communication market include the continuous and rapid increase in data throughput from 4G to 5G and even 6G, with higher base station density and a proportional increase in power management ICs. Increased data throughput also demands greater processing capacity, requiring denser, more efficient power management ICs. The communications industry consumes a significant amount of national electricity, so improving efficiency helps save energy and aligns with the country’s dual-carbon strategy. SCT is deeply involved in enhancing the performance of power management ICs in this field.

3. From a design and development perspective, what is the current state of technological iteration in domestic power management chips? How do they compare to industry leaders such as Texas Instruments?

Liang Junfeng: Compared to TI, ADI, and ST, domestic power semiconductor companies primarily focus on specific product directions. The foreign giants have extensive and complete product systems, offering power management chips for almost every type of device. No domestic chip company currently matches the product coverage of foreign manufacturers.

Another characteristic is that domestic semiconductor companies have been around for a relatively short time, and many have not yet fully iterated their products. Most are still working on improving product categories and expanding market share. This leads to the issue that when new problems arise in different customer markets, domestic companies may not have the resources to iterate quickly.

SCT focuses on mid-to-high voltage power conversion and has already reached the third generation of its products, which places us ahead of many domestic semiconductor companies.

Foreign companies have research labs, institutes, or centers dedicated to observing emerging market fields and investing heavily in new technological directions. Most domestic companies are still in a follow-up stage. Unlike digital chips, which have rapid technological iterations (e.g., every 2 years for 7nm, 5nm, 2nm processes), analog chips have longer iteration cycles. If large analog chip companies fail to continuously develop leading technologies, the pace of catching up from competitors will accelerate.

However, recognizing the gap allows us to set clear goals. By focusing on these goals, we can aspire to catch up with and eventually surpass foreign leaders with collective efforts.

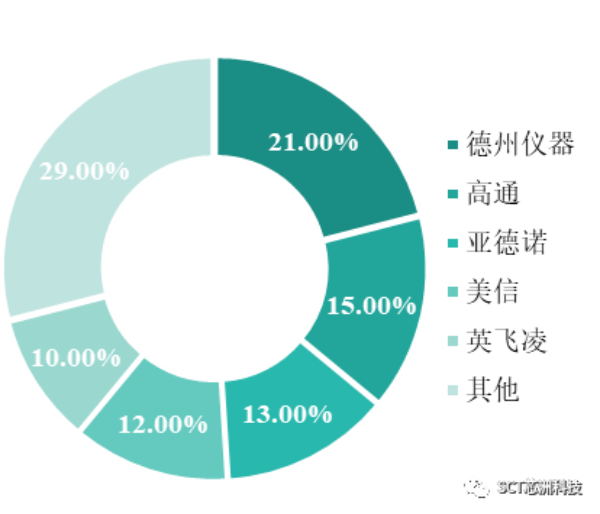

全球电源管理芯片市场竞争格局

数据来源:IC Insights、华经产业研究院

4. Besides technology, what are the breakthroughs and challenges in power management IC manufacturing processes?

Liang Junfeng: For semiconductors, digital chips focus on optimizing process technology to improve processing density. In contrast, analog chips require significant process optimization, especially in terms of research and development cycles, costs, and efficiency. For example, MOSFETs have a standard FOM value, which represents a key metric for power semiconductor technology. Domestic power chips rely on advanced wafer manufacturing processes to improve product performance. In the future, developing proprietary advanced processes or optimizing process capabilities will be essential for domestic IC companies.

SCT enhances product performance through two approaches: 1) addressing customer and market pain points by collaborating with upstream wafer fabs to improve chip designs, and 2) working on process optimization to deliver better performance per unit area.

5. What opportunities and challenges do you see in the industry ecosystem, which may develop horizontally or vertically?

Liang Junfeng: Generally, three types of companies will survive in this market:

Enhancing product categories to fill gaps in the domestic power management chip field. The consumer market has relatively low entry barriers, while other sectors require more advanced solutions, so focusing on filling gaps and then iterating to improve quality is essential.

Continuous product iteration and differentiation to meet customer demands. Once product performance is recognized, iterating to meet specific needs and creating differentiated products will ensure continued success, especially in emerging industries like new energy vehicles, photovoltaics, and edge computing.

Collaborating with the upstream supply chain to enhance semiconductor processes, reduce costs, and improve product performance.

SCT follows this strategic approach: filling domestic product gaps, continuously iterating to meet the needs of key sectors like new energy vehicles, industry, and communications, and collaborating with the supply chain to enhance semiconductor processes. Most importantly, SCT is committed to improving product reliability and quality, offering products that match foreign giants in reliability while continuously developing high-performance products tailored to the domestic market.